Table of Contents

Since the world-wide economic disaster of 2007-09, the sizing of the personal credit history industry has developed dramatically and now exceeds $1 trillion. Antti Suhonen, writer of the review “Immediate Lending Returns,” released in the Money Analysts Journal, examined the returns, risk exposures, and functionality persistence of company growth organizations. BDCs, designed by congressional legislation, are shut-conclude financial investment motor vehicles arranged less than the Financial commitment Corporation Act of 1940. They have the adhering to qualities:

- They commonly spend in compact and midsize companies as a result of personal debt and, to a lesser extent, equity securities and spinoff securities.

- They are demanded to devote at minimum 70% of their property in nonpublic equity and credit card debt of US businesses.

- Suitable investments also contain US federal government securities, income, and detailed securities of providers with a marketplace capitalization of a lot less than $250 million.

- BDC expense holdings are subject matter to diversification specifications.

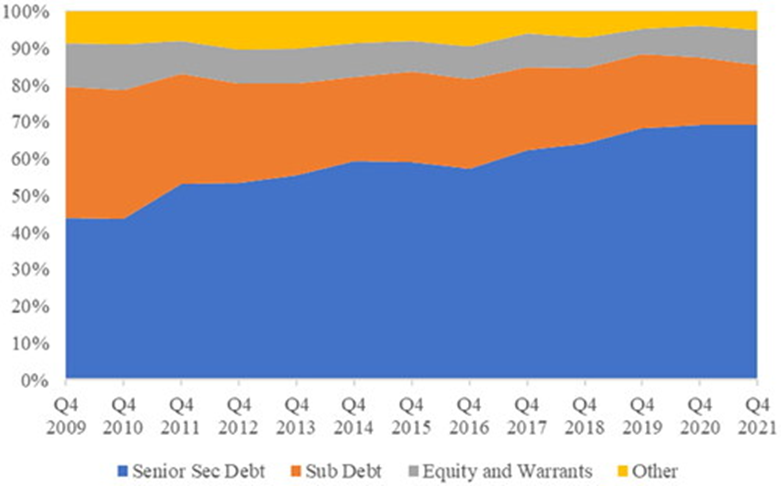

- Senior secured loans form the greater part of BDC portfolio belongings now, while they may well also hold subordinated credit card debt as well as fairness warrants and immediate equity possession in their portfolio firms.

- BDCs are permitted to use up to 200% leverage. Practically all BDCs get benefit of a total change (100%) of leverage. The use of leverage will increase possibility and drawdowns although also rising anticipated returns.

- 90% of a BDC’s income need to be derived from dividends and curiosity, and 90% should be distributed to shareholders.

- Professionals are commonly compensated through a blend of fixed and incentive-based administration charges (percentage of internet curiosity profits and realized gains).

- BDCs are not permitted to concern shares to the community down below web asset value without having yearly shareholder acceptance.

BDCs: Risky and High priced

Suhonen’s database consisted of 47 BDCs (with about $112 billion of assets at the conclusion of 2021) and protected the period of time of December 2009 as a result of June 2022. The following chart displays the industry-capitalization-weighted asset allocation of the 47 BDCs in the sample.

Adhering to is a summary of Suhonen’s essential results:

- BDC portfolio produce averaged 10.8% in excess of the sample period of time (or common USD a few-thirty day period Libor as well as 10%). The yield compressed by 4 percentage points, from a significant of 12.8% in 2012 to 8.6% in initially-quarter 2022, in advance of the widening in the last quarter of the sample. The compression is possible in element a reflection of the advancement in BDC mortgage seniority (see chart). The regular BDC generate distribute about leveraged financial loans all through the sample period of time was 5.7%, ranging concerning .9% and 7.9%.

- Considering the fact that 2019, the financial debt/equity ratio has averaged 102% versus 61% in 2009-17. The increase in leverage is thanks to congressional action taken in 2019 that raised the leverage restrict to 2. from 1..

- The ordinary annual management cost cost (which include incentive expenses) in excess of the sample time period was 3.19% of whole belongings, corresponding to 5.46% of internet belongings. This compares with an ordinary administration payment of 3.14% for each year of internet belongings for personal immediate lending resources.

- The normal funding price was 4.36% per yr of overall credit card debt, or a few-month Libor in addition 3.58% given an regular Libor fee of .78% through the period of time.

- BDC field overall returns at the market-capitalization-weighted index level were being 8.63% per year with a Sharpe ratio of .38. The Sharpe ratio was nicely below that of equivalent benchmarks these kinds of as leveraged loans (.61) and significant-produce bonds (.63).

- BDC current market worth returns had been most effective defined by a mix of liquid leveraged bank loan performance and equity industry, sizing, and price elements.

- Bundling the fairness factors into one particular by working with an equity modest-cap price index as an explanatory variable alongside leveraged financial loans, the two regressors spelled out 81% of BDC marketplace benefit index variation in every month details and resulted in a damaging but statistically insignificant alpha.

- BDCs’ volatility was broadly in line with that of compact-cap equities. Having said that, their returns exhibited much more negative skewness and surplus kurtosis than the fairness benchmarks, nevertheless much less than the leveraged personal loan index.

- Personal BDCs exhibited extensive performance dispersion, with the variation concerning top- and bottom-quartile returns in extra of 15% for every 12 months across different general performance actions.

- Dependent on an NAV return metric, BDC effectiveness exhibited strong 12 months-on-year persistence, specially in the bottom and leading quartiles of previous returns.

- There was a statistically major connection amongst valuation (selling price/NAV) and effectiveness, with BDCs with better cost/NAV top quality (or lesser lower price) outperforming those with a smaller sized high quality (much larger price reduction) by all return metrics.*

Investor Takeaways

The moment traded in the stated marketplace, BDCs undertake the volatility of typical stocks and may deviate from their basic value due to the fact of alterations in investor danger aversion and marketplace liquidity. The final result is that they are riskier than the belongings they hold, a dilemma compounded by their use of high amounts of leverage. Add to that their incredibly higher fees relative to web trader assets (in extra of 5%), and it is tricky to make a case for investing in general public BDCs, especially when there are a lot less risky and significantly less pricey alternate options, such as Cliffwater Corporate Lending Fund CCLFX and Cliffwater Enhanced Lending Fund CELFX. The high price ratio is notably egregious when it is applied to gross property (as opposed to web belongings). The motive is that gross belongings involve those that are financed with leverage that has had an average price tag of about 3.6% over Libor. The consequence is that the trader is paying comprehensive costs on the leveraged assets when they are not earning the comprehensive generate paid by the borrower. In distinction, Cliffwater’s fees are used to net belongings.

*When I reviewed this discovering with Cliffwater’s CEO, Stephen Nesbitt, he informed me that, although the finding was right for a obtain-and-keep system, his analysis discovered that a periodic rebalancing approach from significant selling price/ebook to minimal price tag/e-book made larger returns than a buy-and-maintain tactic.

Larry Swedroe is head of economic and financial exploration for Buckingham Prosperity Partners, collectively Buckingham Strategic Prosperity, LLC and Buckingham Strategic Associates, LLC.

For instructional and informational reasons only and should really not be construed as certain financial investment, accounting, authorized, or tax assistance. Specific data is based mostly on third occasion facts and may turn out to be out-of-date or in any other case outdated without detect. Mentions of precise securities are for instructional functions only and are not suggestions of implementing them into a portfolio. Men and women really should discuss with a experienced economical qualified based on their conditions. Neither the Securities and Exchange Fee (SEC) nor any other federal or condition company have authorised, determined the precision, or confirmed the adequacy of this article. The viewpoints expressed in this article are their have and may possibly not correctly mirror individuals of Buckingham Strategic Prosperity, LLC or Buckingham Strategic Companions, LLC, collectively Buckingham Prosperity Associates. LSR-24-627

Larry Swedroe is a freelance writer. The thoughts expressed in this article are the author’s. Morningstar values variety of believed and publishes a wide range of viewpoints.